"Double carbon" policy has brought about dramatic changes in the power generation structure, and the energy storage market is facing new breakthroughs

Introduction: Driven by the "double carbon" policy to vigorously reduce carbon emissions, the national power generation structure will usher in major changes. By 2030, when carbon peaks, the proportion of new energy power generation will continue to rise to 42%. After 2030, with the improvement of energy storage infrastructure and other supporting equipment, it is expected that by 2060, China will complete the transition from fossil energy power generation to new energy generation. In the transformation of energy power generation, the proportion of new energy power generation will reach more than 80%.

The "dual carbon" policy will drive the pattern of China‘s power generation raw materials from fossil energy to new energy. It is estimated that by 2060, my country‘s new energy power generation will account for more than 80%.

At the same time, in order to solve the "unstable" pressure problem caused by the large-scale grid connection of the new energy power generation side, the "allocation and storage policy" on the power generation side will also bring new breakthroughs to the energy storage side.

"Dual carbon" policy development

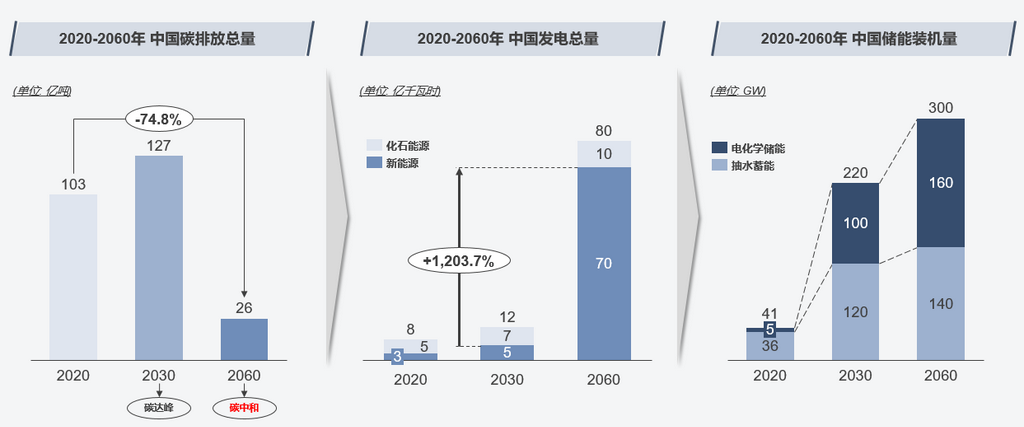

In September 2020, China formally proposed the "dual carbon" goal at the 57th United Nations General Assembly, that is, to achieve "carbon peak" in 2030 and "carbon neutrality" in 2060.

my country strives to reach the peak of carbon dioxide emissions in 2030 and no longer grow. It is estimated that carbon emissions will reach 12.7 billion tons; by 2060, my country‘s carbon emissions will enter the "neutralization" stage, and carbon emissions are expected to be 2.6 billion tons, which is similar to 2020. Year-on-year carbon emissions decreased by 74.8%.

It is worth noting here that "carbon neutrality" does not mean zero emission of carbon dioxide, but the total amount of carbon dioxide or greenhouse gas emissions directly or indirectly generated by corporate production, personal activities, etc., through afforestation, energy conservation and emission reduction. and other forms to offset the carbon dioxide or greenhouse gas emissions generated by itself, achieve positive and negative offset, and achieve relatively "zero emissions".

"Double carbon" strategy drives the change of power generation side pattern

The three major industries with high carbon emissions in my country are: electricity and heating (51%), manufacturing and construction (28%), and transportation (10%).

In the power supply industry with the highest proportion, the national power generation in 2020 will be 800 million kWh, the fossil energy power generation will be nearly 500 million kWh, accounting for 63%; the new energy power generation will be 300 million kWh, accounting for 37% .

Driven by the "double carbon" policy to vigorously reduce carbon emissions, the national power generation structure will usher in major changes.

By 2030, when carbon peaks, the proportion of new energy power generation will continue to rise to 42%. After 2030, with the improvement of energy storage infrastructure and other supporting equipment, it is expected that by 2060, China will complete the transition from fossil energy power generation to new energy generation. In the transformation of energy power generation, the proportion of new energy power generation will reach more than 80%.

The energy storage market ushered in a new breakthrough

With the outbreak of the new energy power generation side market, the energy storage industry has also ushered in new breakthroughs.

Energy storage and new energy power generation (photovoltaic, wind power) are inseparable.

Both photovoltaic power generation and wind power have strong randomness and regional restrictions, resulting in strong uncertainties in the power generation amount and frequency on the power generation side, which will bring great impact pressure on the grid side during the grid connection process. Therefore, the construction of energy storage stations is urgent.

The energy storage station can not only effectively solve the problem of "abandoning solar energy and abandoning wind", but also "peak and frequency regulation" so that the power generation and frequency of the power generation side can fit the planned curve of the grid side, so as to realize the smooth grid connection of new energy power generation.

Compared with foreign markets, my country‘s energy storage market is still in its infancy, with the continuous improvement of my country‘s water conservancy and other infrastructure.

Pumped storage still dominates the market. In 2020, the installed capacity of pumped storage in the Chinese market is 36GW, much higher than the installed capacity of electrochemical energy storage, which is 5GW. However, chemical energy storage has the advantages of being free from geographical restrictions and flexible in configuration. In the future, the growth rate of development is relatively fast; it is expected that in 2060, my country‘s electrochemical energy storage will gradually surpass the installed capacity of pumped storage, reaching 160GW.

At this stage, in the bidding of new energy power generation side projects, many local governments will clearly stipulate that the allocation and storage of new energy power stations should not be less than 10%-20%, and the charging time should not be less than 1-2 hours. It can be seen that the "distribution and storage policy" will be The electrochemical energy storage market on the power generation side has brought very considerable growth.

However, at this stage, the profit model and cost transfer of electrochemical energy storage on the power generation side are not yet very clear, resulting in a low internal rate of return.